If you need an ITIN for a nonresident alien spouse in 2026, navigating the IRS process can quickly become overwhelming. To file a joint tax return and access the financial benefits that come with it, your spouse may need an Individual Taxpayer Identification Number (ITIN).

On paper, the IRS process looks straightforward. In practice, international couples often face tax software errors that block filing, long passport processing delays, unexpected global reporting obligations, and a complex tax election that can significantly change how both spouses are taxed.

This guide bridges the gap between official IRS rules including the latest Form W-7 Instructions, Publication 519, and IRS.gov guidance and the real world operational steps needed to improve your chances of approval on the first submission.

Important: The Section 6013(g) election can trigger worldwide income taxation and foreign account reporting obligations such as FBAR and FATCA. Couples with foreign income, foreign investments, or overseas financial accounts should strongly consider consulting a CPA experienced in cross-border taxation before filing jointly.

Official sources used: Form W-7 Instructions | Publication 519 | Nonresident Spouse Election | IRS ITIN page | About Form W-7

Can You Get an ITIN for a Nonresident Alien Spouse in 2026?

Yes, regardless of immigration status, visa type, or physical location. The IRS explicitly states that nonresident aliens and their spouses can apply for an ITIN regardless of immigration status, provided they have a valid federal tax purpose.

A nonresident alien spouse qualifies when they are filing a joint US tax return or being claimed for an allowable tax benefit. A B-2 tourist visa, a spouse who has never entered the US, or a spouse currently living abroad none of these disqualify someone from getting an ITIN.

The IRS explicitly names these allowable tax benefits for spouses in the Form W-7 Instructions:

- Filing a joint return (Married Filing Jointly) the most common reason

- Head of Household (HOH) with important restrictions for nonresident alien spouses (see Publication 501)

- Qualifying Surviving Spouse (QSS)

- American Opportunity Tax Credit (AOTC)

- Premium Tax Credit (PTC)

- Child and Dependent Care Credit (CDCC)

- Credit for Other Dependents (ODC)

For most couples, filing a joint return after making the residency election is the primary reason for a spouse ITIN application.

Post-2017 rule: For tax years after December 31, 2017, a nonresident alien spouse is NOT eligible for an ITIN or ITIN renewal unless they are claimed for one of the above allowable tax benefits or they file their own US tax return. The old practice of listing a nonresident spouse simply to claim a personal exemption no longer qualifies personal exemptions are currently $0.

Which Box on Form W-7 Does a Spouse Check?

A nonresident alien spouse checks Box e on Form W-7.

The exact IRS language for Box e is:

“Spouse of U.S. citizen/resident alien. This category includes: A resident or nonresident alien spouse who isn’t eligible to get an SSN but who is electing to file a U.S. federal tax return jointly with a spouse who is a U.S. citizen or resident alien.”

(Form W-7 Instructions, Reason You’re Submitting Form W-7)

Warning: Do not check box d. Box d is for dependents. Your spouse is never a dependent under IRS rules. The IRS explicitly states: “Your spouse is never considered your dependent.” Using the wrong box is one of the most common rejection causes and requires a complete re-application.

See also: How to Get an ITIN for a Child, Parent, or Dependent in 2026

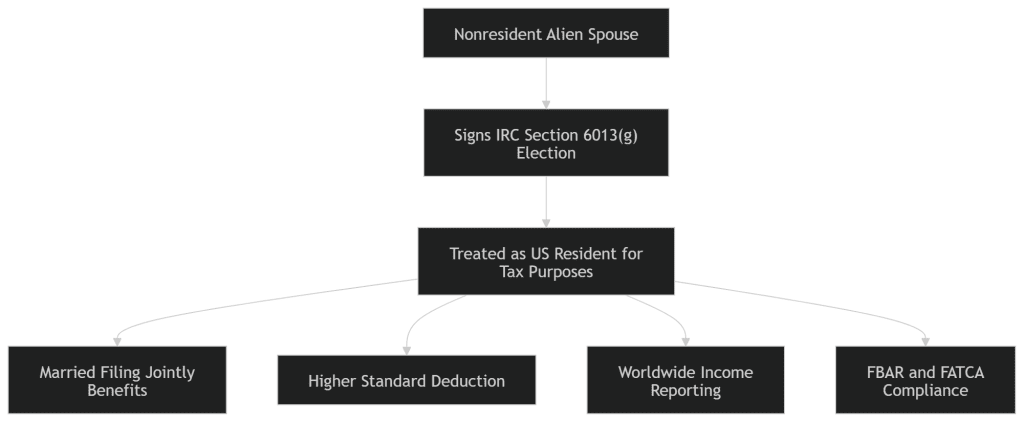

Understanding the IRC Section 6013(g) Resident Election

To file a joint return with a nonresident alien spouse, you must invoke Internal Revenue Code Section 6013(g). This is a legal declaration where you choose to treat your nonresident spouse as a US resident alien strictly for tax purposes.

[Nonresident Alien Spouse]

│

▼ (Earns foreign income abroad)

[Signs Section 6013(g) Resident Election]

│

▼ (Legal transformation for tax purposes only)

[Deemed US Resident Alien for Tax Year]

│

├─► BENEFIT: Married Filing Jointly brackets

├─► BENEFIT: Higher standard deduction

└─► LIABILITY: Worldwide income taxed + FBAR/FATCA reporting

What the Election Does

When you make this election, both you and your spouse are treated as US residents for the entire tax year for income tax purposes. Publication 519 states explicitly:

“If you make this choice, you and your spouse are treated for income tax purposes as residents for your entire tax year. You are both taxed on worldwide income.”

This is the most critical detail most articles skip. Once the election is made, your spouse’s income from any country salary, rental income, investments, foreign pensions becomes reportable on your joint US Form 1040.

What Most ITIN Articles Get Wrong

Most online guides explain how to submit Form W-7 but skip the financial consequences of the Section 6013(g) election. The real complexity is not getting the ITIN approved it is understanding that filing jointly can expose a spouse’s worldwide income and foreign financial accounts to US reporting requirements.

For some couples, filing jointly saves thousands in taxes. For others, the additional FBAR, FATCA, and international compliance obligations can outweigh the tax benefits entirely.

Before making the election, compare the total tax impact of Married Filing Jointly versus Married Filing Separately and consider speaking with a CPA experienced in international tax compliance.

What Form You File

When making the election, you file Form 1040 (not Form 1040-NR). You file jointly for the year you make the election. The election is not available on a separate return.

How to Make the Election Exact Steps

Step 1: Prepare your joint Form 1040 for the tax year.

Step 2: Write a signed statement signed by both spouses with original handwritten signatures and attach it to the front of the return. The statement must include:

- A clear declaration that you are making the election under IRC Section 6013(g) to treat the nonresident spouse as a US resident for the tax year

- The full legal name, address, and taxpayer identification number of each spouse

- The specific tax year for which the election applies

- Note: Your spouse’s TIN field in the statement can reference “ITIN applied for” if the application is pending

Step 3: Attach Form W-7 to the front of the return. Leave the SSN/ITIN field blank on Form 1040 for the spouse the IRS explicitly instructs this.

Step 4: Mail the complete package to the IRS ITIN Operation in Austin. You cannot e-file this return.

Is the Election Permanent?

No. This is one of the most common pieces of misinformation circulating in immigration forums. The election can be suspended or revoked under specific circumstances detailed in Publication 519.

The actual IRS rule is this: once the election is ended or revoked for a specific marriage, neither spouse can make the election again for that same marriage. However, if either person remarries in the future, the new marriage is treated independently the restriction applies to the same marital relationship, not to the individuals for life.

Correct framing: The election is a significant commitment that affects how you are taxed for the year it is made and all subsequent years unless revoked. It is not something to make casually. But it is not an irreversible lifetime decision. Review Publication 519’s suspension and revocation rules before deciding.

Worldwide Income and Foreign Asset Reporting Risks

Most online articles about spouse ITINs stop at “file jointly and save money.” That is incomplete advice. Before making the Section 6013(g) election, you need to understand the full financial exposure.

Worldwide Income Reporting

The moment your spouse is treated as a US resident for tax purposes, their global income is added to your joint Form 1040. This includes:

- Salary or wages earned in their home country

- Rental income from property abroad

- Interest and dividends from foreign bank accounts

- Foreign government pension payments

- Business income from a foreign-registered company

For spouses with modest foreign income, the joint filing tax savings usually outweigh the additional reporting. For spouses with substantial foreign income especially those in high-income countries the math often reverses.

Run the numbers before committing. Calculate your combined tax under Married Filing Jointly with the election against Married Filing Separately without it. For many H-1B holders with spouses back in India, the UK, or Canada earning professional salaries, MFS costs less in total taxes despite the higher individual rate.

The FBAR Trap

Once your spouse is classified as a US resident for tax purposes under the election, they fall under US foreign bank account reporting requirements. Specifically:

If your spouse holds foreign bank accounts individually or jointly where the aggregate balance exceeds $10,000 at any point during the calendar year, they must file FinCEN Form 114 (FBAR) with the Financial Crimes Enforcement Network by April 15 of the following year (with automatic extension to October 15).

This covers:

- Personal savings and checking accounts abroad

- Foreign brokerage accounts

- Accounts held jointly with family members in their home country

- Provident fund accounts (in countries like India) this is contested but commonly reported

These penalties are adjusted periodically for inflation and can become severe even for accidental noncompliance.

The FBAR penalty structure for 2026:

- Non-willful violation: up to $16,536 per report per year (2026 inflation-adjusted)

- Willful violation: the greater of $165,361 or 50% of the account balance per violation

Most couples making the 6013(g) election are unaware of FBAR until they are already exposed. Many discover it after the first joint return is filed and a tax professional asks about the spouse’s foreign accounts.

Related: FBAR for Immigrants: A 2026 Guide for Foreign Bank Accounts

The FATCA Threshold

If your spouse’s total foreign financial assets exceed specific thresholds, they must also file Form 8938 (FATCA) with their tax return:

- Single or Married Filing Separately living in the US: over $50,000 at year end or $75,000 at any point

- Married Filing Jointly living in the US: over $100,000 at year end or $150,000 at any point

- Living abroad: thresholds double

For many immigrant couples with spouses in countries like India, the UK, or Australia who have accumulated savings, retirement accounts, or property investments, these thresholds are reachable.

Bottom line: The tax savings of filing jointly can be completely wiped out by international compliance costs. If your spouse has any meaningful foreign assets or income, consult a CPA who specializes in cross-border taxation before making the election.

Who Should Think Carefully Before Filing Jointly

The Section 6013(g) election may not be beneficial if your spouse:

- Earns substantial foreign income

- Holds large foreign investment or brokerage accounts

- Owns foreign businesses, corporations, or partnerships

- Has significant retirement or pension assets abroad

- Could trigger costly FBAR or FATCA reporting obligations

For some couples, Married Filing Separately results in lower overall compliance costs despite the less favorable tax brackets.

Married Filing Separately The Alternative Path

If the worldwide income exposure or the FBAR and FATCA reporting requirements create too much liability, you can bypass the joint election entirely by filing as Married Filing Separately.

Under this approach:

- You file Form 1040 as Married Filing Separately

- Your nonresident alien spouse files Form 1040-NR only if they have US-sourced income that requires reporting

- Write “NRA” in the entry space for your spouse’s Social Security Number on your Form 1040

Publication 519 explicitly confirms the NRA entry:

“If your spouse doesn’t have and isn’t required to have an SSN or ITIN, enter ‘NRA’.”

Under MFS, your spouse is taxed only on US-sourced income not worldwide income. Without the residency election, a nonresident alien spouse generally does not become subject to FBAR reporting solely because the US citizen or resident spouse files separately. The tradeoff is higher individual tax rates and the loss of certain credits available only to joint filers.

Software trap for MFS: Most consumer tax software platforms will block you from typing “NRA” directly into the hardcoded SSN field. Use the same PDF redaction method described below to print NRA cleanly on the physical paper return.

Related: ITIN vs SSN in 2026

Step by Step Implementation and the Software Workaround

Because a first-time ITIN application requires a physical tax return attached to it, you cannot e-file. This creates a direct conflict with every major tax software product on the market.

Step1: The Print and Override Method

The IRS instructs you to leave the SSN area blank for the person applying for an ITIN. However, TurboTax, H&R Block, FreeTaxUSA, and most other software platforms will throw a critical diagnostic error and block you from finalizing the return if any SSN field is empty.

Here is the practical workaround used by international tax professionals:

- Enter a temporary placeholder SSN (such as 999-99-9999) into the software to clear the diagnostic block and allow you to finalize all forms.

- Before printing, use the software’s “Print for Mail” or “Form View” mode to delete the temporary number. If your software hardcodes the number into the final PDF, use a PDF editor to digitally blank out the SSN field before printing.

- Do not use physical white-out or correction fluid on the printed return. IRS scanning equipment routinely flags returns with liquid correction products as potential document tampering. The field must print clean and blank.

- The final printed Form 1040 that goes into your mailing package must show the spouse’s SSN field completely blank no numbers, no placeholder text, no white-out marks.

Step 2: Draft the Election Statement

The IRC Section 6013(g) election statement is a standalone typed document. The IRS does not provide a form for this you create it yourself. It must contain:

- Title: “Election to Treat Nonresident Alien Spouse as US Resident Under IRC Section 6013(g)”

- Tax year of the election

- Full legal name of both spouses exactly as they appear on their identity documents

- US address and foreign address of each spouse

- SSN of the US citizen/resident spouse

- ITIN field for the nonresident spouse (write “Applied For” if pending)

- Declaration: a sentence stating you are making this election for the specified tax year

- Original handwritten signatures of both spouses and the date

Step 3: The Handwritten Signature Requirement

For Form W-7 applications and Section 6013(g) election statements, original handwritten signatures are generally required.

- Digital signatures via DocuSign or Adobe Sign are generally not accepted

- Printed scans of a signed document may create processing issues

- If your spouse is overseas, mail the physical unsigned documents to them, they sign in blue or black pen, and they mail the physically signed originals back to you via trackable courier (DHL or FedEx recommended)

This round-trip signature process typically adds 2–3 weeks to your preparation timeline. Build this into your schedule before the tax filing deadline.

Step 4: Assemble the Package in This Exact Order

Stack your physical package from top to bottom in this sequence before sealing the envelope:

- Form W-7 with original handwritten signature on top

- Identity documents original passport or CAA certification

- Form 1040 with spouse SSN field completely blank

- Section 6013(g) Election Statement with original handwritten signatures from both spouses

- All supporting schedules, W-2s, 1099s, and any applicable forms

Do not use staples through the entire package. Use a binder clip or paperclip to keep pages organized. Staple marks through multiple documents can cause scanning issues at the IRS processing center.

Supporting Documents and the Passport Decision

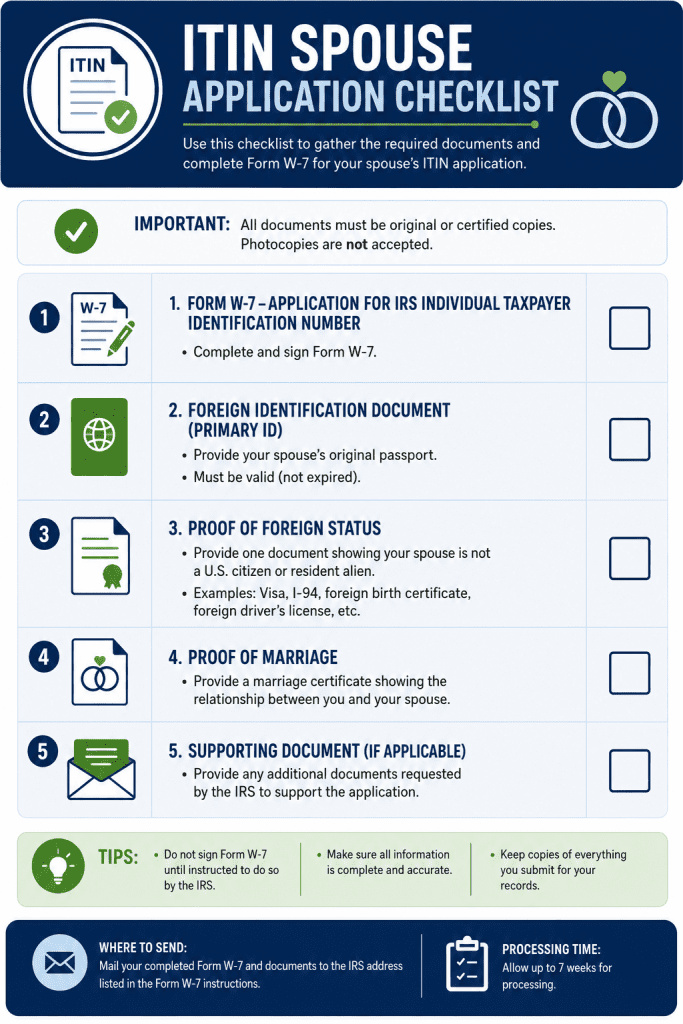

To clear Form W-7 screening, your spouse must prove both identity and foreign status.

Passport the only standalone document

A valid, unexpired passport establishes both identity and foreign status simultaneously. If your spouse has a valid passport, it is the only document required for the W-7 supporting documentation requirement.

No passport two documents required

Without a passport, submit at least two documents from the IRS list of 13 acceptable items. A national ID card plus a foreign driver’s license or a foreign military ID card are common combinations.

Spouse has never entered the US

Write “Never entered the United States” on Line 6d of Form W-7. This is explicitly permitted by the IRS and does not hurt the application in any way.

The Original Passport Risk

The IRS requires original documents or certified copies from the issuing agency. Do not mail your spouse’s original passport directly to Austin, Texas.

Real-world processing times from r/ITIN, r/tax, and r/immigration consistently show 14–20+ weeks during peak season for international submissions. That means your spouse could be without their passport unable to travel internationally for nearly half a year. The IRS does aim to return documents within 60 days of receipt, but returns arrive separately from the ITIN notice and tracking is limited once inside the IRS system.

The CAA Solution

Instead of mailing the original passport, use an IRS-authorized Certifying Acceptance Agent (CAA). A CAA is a tax professional licensed by the IRS to physically verify, authenticate, and certify original foreign passports. They complete Form W-7 (COA), attaching their certification so your original passport never leaves your spouse’s possession.

Important operational rule: A CAA cannot verify a passport remotely. Your spouse must appear in person with their original passport at the CAA’s office. If your spouse is overseas, they must find a CAA located in their home country you cannot bring their passport to a US-based CAA on their behalf.

Note on US Embassies and Consulates: While the IRS states that US Embassies and Consulates can certify passport copies for ITIN purposes, real-world reports from immigration forums indicate that many consulates have shifted away from providing this service, referring applicants to international CAAs instead. Contact your nearest US Embassy or Consulate directly before relying on this option.

Find a CAA at IRS.gov by searching the Acceptance Agent Program directory. Search by country to find agents in your spouse’s home country.

ITIN for Nonresident Alien Spouse 2026 Processing Times

| Submission Window | Official IRS Estimate | Real-World Reports (2026) |

|---|---|---|

| Off-peak (May – December) | Approximately 7 weeks | 8–12 weeks |

| Peak tax season (Jan 15 – Apr 30) | 9 to 11 weeks | 14–20 weeks |

| International mail submissions | 9 to 11 weeks | 16–22 weeks |

Official estimates are from the Form W-7 Instructions. Real world reports from r/ITIN, r/tax, and r/immigration consistently show longer timelines, particularly for applications originating from South Asia during peak season.

Travel warning: If your spouse mailed their original passport, do not plan any international travel requiring that passport for at least 14–16 weeks after mailing. Original documents are returned separately from the CP565 notice and cannot be tracked once received by the IRS ITIN Operation.

After your application is processed you will receive one of three notices:

CP565 ITIN approved and assigned. Your Form 1040 is released to the standard processing queue. No further action needed.

CP566 Additional information required. You have a limited window to respond with the requested documentation before the application is cancelled. Respond immediately.

CP567 Application rejected. The notice explains the specific failure missing signature, uncertified copies, wrong box, missing return. You must reapply from scratch with a corrected package.

If you have not received any notice after 11 weeks (off-peak) or 14 weeks (peak season): Call the IRS ITIN hotline. Call early in the morning the first two hours after opening give you the best chance of reaching a live agent. Have your tracking number from the USPS or courier shipment ready.

ITIN Renewal Rules for Spouses

If your spouse’s ITIN has not been used on a US federal tax return for three consecutive years, it may become inactive and require renewal before filing again.

The Form W-7 Instructions state:

“All Form W-7 renewal applications must include a U.S. federal tax return unless you meet an exception. Spouses and dependents who renew their ITIN must be listed on an attached U.S. federal tax return with the schedule or form that applies to the allowable tax benefit.”

When your spouse later gets an SSN: Stop using the ITIN immediately. Once your spouse receives a valid SSN for example, after changing to a work-authorized visa status they must use the SSN on all future returns. The IRS explicitly states: “If you received your SSN after previously using an ITIN, stop using your ITIN. Use your SSN instead.”

Most Common Rejection Reasons

Wrong box checked: Box d is for dependents. Box e is for spouses. These are different categories with different rules. A spouse filing under box d will be rejected.

Missing or invalid election statement: The 6013(g) statement must be typed, include all required information, and carry original handwritten signatures from both spouses.

No tax return attached: Form W-7 for a spouse must be filed with an attached tax return. Do not submit W-7 alone unless you qualify for a specific exception which most spouse applicants do not.

Name mismatch: The legal name on the W-7 must exactly match the name on the supporting identity documents and on the tax return. Nicknames, shortened names, or maiden name inconsistencies all cause delays or rejection.

P.O. box on Line 2 with only a country name on Line 3: The IRS explicitly states this combination will result in rejection.

White-out on the printed return: Do not use liquid correction fluid anywhere on your tax return or W-7. IRS scanning equipment flags this.

One spouse signing for the other: Each person must sign their own Form W-7 unless a valid Power of Attorney (Form 2848) is attached.

Attempting to e-file: Any return attached to a first-time W-7 must be paper filed. The ITIN does not exist yet and cannot be processed through e-file systems.

Submission Checklist Before Mailing

Use this before sealing your envelope:

- Box e checked on Form W-7 (not box d)

- Line 6d completed date of entry or “Never entered the United States”

- Spouse SSN field on Form 1040 is completely blank no temporary numbers, no white-out

- Election statement typed, includes all required information, signed by both spouses

- Original passport or CAA certification included

- Form W-7 placed on the absolute top of the package

- No white-out anywhere in the package

- Package sent to Austin ITIN Operation address not the standard 1040 mailing address

- Sent via trackable mail (USPS certified, FedEx, or DHL)

- Copy of the entire package kept before mailing

- Spouse’s foreign accounts reviewed for FBAR threshold ($10,000 aggregate)

- FATCA threshold reviewed if spouse has foreign financial assets

ITIN for Nonresident Alien Spouse 2026 FAQs

Can my spouse get an ITIN if they have never been to the US?

Yes. Write “Never entered the United States” on Line 6d of Form W-7. There is no IRS rule requiring US presence for a spouse ITIN. Many spouses apply successfully from abroad and receive approval.

Does visa type affect eligibility?

No. The IRS grants ITINs regardless of immigration status. A spouse on a B-2 tourist visa, a student visa, or no US visa at all can apply for an ITIN provided there is a valid tax purpose which filing jointly satisfies.

Is the 6013(g) election permanent?

No. The election can be suspended or revoked. The restriction is that once ended for a specific marriage, it cannot be made again for that same marriage. A new marriage is treated independently. See Publication 519 for the complete suspension and revocation rules.

What if my spouse earns a high salary abroad?

Run both scenarios before deciding. If your spouse earns significant income in a country with lower tax rates than the US, making the election could result in a higher combined tax bill than filing separately. Consult a cross border tax specialist before filing.

Can a CAA in India, Nepal, or the UK handle this?

Yes. CAAs operate internationally. Your spouse must appear in person at the CAA’s location with their original passport. Search the IRS CAA directory by country at IRS.gov.

What about FBAR if we only file jointly for one year then revoke?

The FBAR obligation applies for the year the election is in effect. If you make the election for 2026, your spouse’s foreign accounts for calendar year 2026 are subject to FBAR if over $10,000. Revoking for 2027 means the 2027 accounts are not covered — but the 2026 FBAR must still be filed.

What do I write in the spouse SSN field on Form 1040?

Leave it completely blank. The Form W-7 Instructions explicitly state to leave the SSN area blank for each person applying for an ITIN. Do not write “Applied For,” “Pending,” or any placeholder text.

Related Guides

- How to Get an ITIN for a Child, Parent, or Dependent in 2026

- Can You Get an ITIN on a Tourist Visa (B-1/B-2) in 2026?

- ITIN vs SSN in 2026: What You Need to Know

- How to Apply for an ITIN in 2026

- FBAR for Immigrants: A 2026 Guide for Foreign Bank Accounts

This article provides general educational information based on the latest available IRS Form W-7 Instructions, Publication 519, and IRS.gov guidance available at the time of writing. It does not constitute formal tax or legal advice. The worldwide income implications and FBAR/FATCA compliance obligations of the Section 6013(g) election can be significant consult a licensed CPA or tax attorney specializing in cross-border and immigration taxation before making this election.