OPT taxes catch thousands of F-1 students off guard every year and the consequences go beyond a missed payment. This guide covers every rule F-1 students on OPT must know FICA exemptions, Form 1040-NR filing, STEM OPT restrictions, and tax treaty benefits by country.

📋 Key Sources

What Are OPT Taxes and Who Has to Pay Them?

Optional Practical Training (OPT) is temporary employment authorization that allows F-1 students to work in jobs directly related to their major. You can use it before graduation (pre-completion OPT) or after (post-completion OPT).

The moment you earn wages in the United States, the IRS gets involved regardless of your visa status. You are earning US-source income, and that triggers a federal tax filing obligation.

Resident Alien or Nonresident Alien? This Determines Everything

Your tax residency status is separate from your immigration status. You can be on an F-1 visa and still be classified as a US resident for tax purposes. The IRS uses the Substantial Presence Test (SPT) to make this determination.

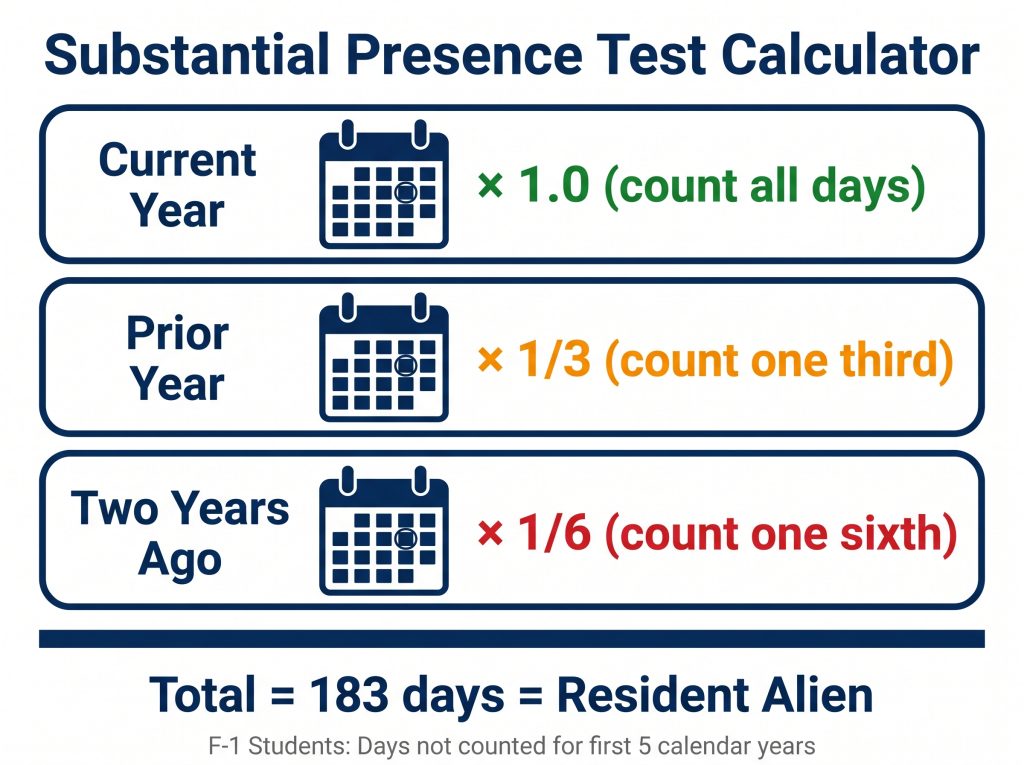

The Substantial Presence Test Formula

You are a US resident alien if you were physically present in the US for:

- At least 31 days in the current year, AND

- At least 183 weighted days over the past 3 years

Total = (All days this year) + (1/3 of days last year) + (1/6 of days two years ago)

The F-1 Exemption: You Don’t Count Days for 5 Years

F-1 students are “exempt individuals” for SPT purposes. Your days in the US do not count toward the 183-day threshold for your first 5 calendar years.

⚠️ Critical: This is a lifetime limit, not a per-program limit. If you were in the US on an F-1 visa in high school from 2018 to 2020, those years count. A student returning for a Master’s in 2024 may have already exhausted their exempt years. Do not assume you are starting from Year 1.

⚠️ Calendar Year Rule: Any portion of a year counts as a full year. Arriving in December 2021 counts as Year 1 not a partial year.

| Year of F-1 US Presence | SPT Day Count | Tax Status |

|---|---|---|

| Years 1–5 (F-1 exempt) | Days NOT counted | Nonresident alien |

| Year 6 onward | Days counted toward SPT | Likely resident alien |

The FICA Exemption: No Social Security or Medicare Tax

Social Security and Medicare taxes (FICA) take 7.65% out of every American worker’s paycheck. As an F-1 student on OPT who remains a nonresident alien, you are exempt from both.

This exemption under IRC Section 3121(b)(19) covers:

- On campus employment

- Curricular Practical Training (CPT)

- Pre completion OPT

- Post completion OPT

- STEM OPT 24-month extension as long as you remain a nonresident alien

✅ Note: Your employer is also exempt from their matching 7.65% FICA contribution while you are covered. This is a direct financial incentive for US companies to hire international STEM talent.

Once you become a resident alien in Year 6+, the FICA exemption ends for off-campus OPT employment and your employer begins withholding immediately.

⚠️ If your employer withholds FICA in error: Request a refund directly from them first. If they refuse, file Form 843 with the IRS with your W-2, passport visa stamp, I-94, and Form 8316.

Which Tax Form Do OPT Students File?

| Your Status | Form to File |

|---|---|

| Nonresident alien (most OPT students, Years 1–5) | Form 1040-NR |

| Resident alien (Year 6+, met SPT) | Form 1040 |

| Transition year | Dual-status return |

Form 1040-NR: Key Rules

As a nonresident alien on OPT:

- You cannot claim the standard deduction (Indian students are the exception covered in the treaty section below)

- You cannot file jointly with a US citizen spouse without making a specific tax election. If you’re married to a US citizen or green card holder, the nonresident alien spouse tax election changes your entire filing strategy

- You must report all US-source income

Filing Deadline

April 15, if you earned wages on OPT, your employer is your withholding agent. You file by April 15 even if $0 was actually withheld due to a treaty. The June 15 deadline applies only to those whose sole US income was not subject to any withholding arrangement which does not apply to employed OPT students. When in doubt, treat April 15 as your hard deadline.

For a full walkthrough of what nonresidents actually owe and how to complete the form, see the Form 1040-NR filing guide.

Form 8843: File It Every Year, No Exceptions

Every F-1 student present in the US during the calendar year must file Form 8843 even with zero income.

⚠️ The Real Risk is Immigration, Not Just Tax: Failing to file Form 8843 does not carry a direct monetary IRS penalty if no tax is owed. The actual danger is that USCIS can treat the failure as evidence you are not maintaining your visa status which can jeopardize any future visa renewal, H-1B petition, or green card application. File it every year without exception.

File Form 8843 by the same deadline as your Form 1040-NR.

Tax Treaty Benefits: Does Your Country Have a Deal With the US?

The US has bilateral tax treaties with dozens of countries that give F-1 students reduced rates or full exemptions on certain income. Your country of citizenship determines what you can claim.

| Country | Treaty Article | Benefit | Residency Limit |

|---|---|---|---|

| China | Article 20(c) | $5,000/year wage exemption | Continues even as resident alien |

| India | Article 21(2) | Standard deduction ($15,750 for 2025 income / $16,100 for 2026 income) | Nonresident alien only |

| South Korea | Article 21(1) | $2,000/year exemption | 5 years |

| Canada | Article XV | Income exempt only if total stays under $10,000 | No limit (under threshold) |

| Germany | Article 20(4) | $9,000/year exemption | 4 years |

| France | Article 21(1) | $5,000/year exemption | 5 years |

✅ Chinese students read this carefully: Article 20(c) is the only major treaty that survives the transition to resident alien status. Every other country’s student treaty benefits disappear once you meet the Substantial Presence Test. Chinese students in Year 6, 7, or 8 can still claim the $5,000 wage exemption. This is the single most valuable and least-known advantage in international student tax law.

⚠️ Canadian students the cliff rule: The Article XV exemption is not a deduction. It is a threshold. If you earn $9,999, you owe nothing. If you earn $10,001, you owe tax on the entire amount from dollar one not just the amount above $10,000. Plan your income accordingly.

✅ Indian students: Article 21(2) of the US-India treaty allows you to claim the standard deduction on Form 1040-NR a benefit normally reserved for US citizens and residents. Use the correct figure for the tax year you are filing: $15,750 for 2025 income, $16,100 for 2026 income.

How to Claim Treaty Benefits

- For wages: Give your employer Form 8233 must be renewed annually

- For scholarships or fellowships: Provide Form W-8BEN

- If your treaty position conflicts with the Internal Revenue Code: File Form 8833 with your tax return

Self-Employment on OPT: One Rule That Will Get You Deported If You Miss It

This is where most guides fail international students, and the consequences go beyond taxes.

Standard Post-Completion OPT (12 months): Self-Employment Allowed

During your initial 12-month post-completion OPT, you may work as a freelancer, independent contractor, or run your own business only if the work is directly related to your degree field and you actively work at least 20 hours per week. Passive ownership is not enough.

STEM OPT Extension (24 months): Self-Employment Is Prohibited:

⚠️ Warning: Freelance and 1099 work are prohibited during the 24-month STEM OPT extension. However, self employment through business ownership is allowed under strict conditions all of the following must be true simultaneously:

- You own the majority of the business

- The business is enrolled in E-Verify

- You maintain a bona fide employer employee relationship with the business

- A signed Form I-983 training plan is on file

- You actively work at least 20 hours per week passive ownership alone does not qualify

If any one of these conditions is not met, you are in violation of your immigration status. This is not a gray area it is a visa revocation risk.

| OPT Type | Freelance/1099 | Business Ownership |

|---|---|---|

| Standard post-completion OPT (12 months) | ✅ Allowed | ✅ Allowed degree related, 20+ hrs/week |

| STEM OPT extension (24 months) | ❌ Prohibited | ✅ Allowed only if all 5 conditions met |

Tax Treatment of Self-Employment Income

| Status | Self-Employment Tax | Income Tax |

|---|---|---|

| Nonresident alien (Years 1–5) | Not owed | Owed on US-source income |

| Resident alien (Year 6+) | 15.3% owed | Owed on worldwide income |

If you’re on standard OPT and earning freelance income from foreign clients, the self-employment tax exemption as a nonresident alien is significant. The situation changes entirely if you have already transitioned to resident alien status in Year 6 that same income now carries a 15.3% self-employment tax in addition to income tax. Once you become a resident alien in Year 6, you also trigger FBAR reporting obligations if you hold foreign bank accounts exceeding $10,000. See the FBAR guide for immigrants before that transition hits.

Penalties for Non-Compliance

| Violation | Penalty |

|---|---|

| Failure to file Form 1040-NR | 5% of unpaid tax per month, up to 25% |

| Return more than 60 days late | Minimum $525 or 100% of unpaid tax (whichever is less) |

| Failure to file Form 8843 | Immigration status risk; potential loss of treaty benefits |

| Incorrect treaty claim | Back taxes + interest + potential fraud flags |

| Self-employment on STEM OPT | Visa revocation, SEVIS termination |

OPT Tax Compliance Checklist

Follow this checklist to stay fully compliant with your OPT taxes obligations.

- Determine your total F-1 calendar years in the US: include any prior F-1 presence, even from high school or a previous program

- File Form 8843: every year, regardless of income

- Check your country’s tax treaty: submit Form 8233 to your employer before your first paycheck

- Verify your employer is not withholding FICA: if they are, correct it immediately

- Track all US-source income: wages, freelance income, taxable scholarships

- File Form 1040-NR by April 15: do not rely on the June 15 date if you have an employer

- STEM OPT students: do not freelance, do not form an LLC, do not take 1099 work under any circumstances

Frequently Asked Questions

Do I owe Social Security tax on OPT income?

No, F-1 students on OPT remain exempt from FICA taxes as long as they are nonresident aliens typically through their first 5 calendar years of US presence. The exemption applies to STEM OPT as well, but only while nonresident alien status holds.

Does the 5 year F-1 exemption reset between programs?

No. It is a lifetime limit. Every calendar year you spent in the US on an F-1 visa including high school, community college, or a previous undergraduate degree counts toward the 5 year limit.

What happens to my taxes in Year 6?

You begin counting days toward the Substantial Presence Test, If you meet the 183-day threshold, you become a resident alien meaning Form 1040, FICA taxes, and worldwide income reporting. Plan for a significant tax increase in Year 6.

Can I use TurboTax as an OPT student?

No. TurboTax does not support Form 1040-NR or treaty exemptions. Using it as a nonresident alien typically results in filing Form 1040 incorrectly, which immigration authorities can treat as a fraudulent return. Use Sprintax or a CPA who specializes in nonresident alien returns.

If my employer withheld FICA by mistake, how do I get it back?

Request a refund from your employer first. If they refuse, file Form 843 with the IRS along with your W-2, passport, I-94, and Form 8316.

My treaty exemption means $0 was withheld. Do I still file by April 15?

Yes. Having a withholding agent your employer means your deadline is April 15 regardless of whether any tax was actually withheld. File on time.

Can I file jointly with my US citizen spouse while on OPT?

You can, but it requires a specific election that treats you as a US resident for the entire tax year which has significant implications for how your worldwide income is taxed. The mechanics of that election are covered in the nonresident alien spouse guide.

Does my tax treaty benefit apply automatically?

No. You must actively claim it by submitting Form 8233 to your employer each year. If withholding already occurred, claim the treaty benefit on your Form 1040-NR at filing time.

Legal Disclaimer: This article is for general informational purposes only and does not constitute tax, legal, or immigration advice. Tax laws, IRS regulations, and USCIS rules are complex and subject to change. Consult a qualified US tax professional experienced with nonresident alien returns before making any filing decisions.